SBA loan qualification is an important step for new entrepreneurs trying to get an idea off the ground. Although the SBA specializes in small business lending, not every borrower will qualify for an SBA loan for various reasons, including those outside their control. This article will review the key considerations for obtaining SBA financing, including the “Four Cs” of credit approval (Credit, Collateral, Capacity, and Character).

What does the SBA provide?

Since its founding in 1953, the SBA has worked to protect the interests of small business owners by enabling competitive free enterprise in order to strengthen our national economy. To that end, the SBA facilitates direct bank lending to small businesses by guaranteeing a portion of the bank loan. Traditionally, banks make loans at a discount to the Tangible Asset Value (collateral). For example, if a piece of real estate appraises for $100,000, a banker might lend up to 75% of the appraised value. The 25% discount creates a reasonable “margin of safety” that allows the bank to resell the property quickly if the borrower defaults. Alternatively, the SBA supports small business lending by guaranteeing 75% to 85% of the bank’s loan. This guarantee thus reduces the borrower’s collateral requirement, making it easier to qualify for SBA financing. The guarantees and standardization of SBA loans also support a liquid secondary market where lenders and investors can quickly buy and sell existing loans.

Is there a minimum Credit Score (Credit)?

Ideally, you want to have a Credit Score that’s at least 680 or better. However, some lenders will accept a lower score on a case-by-case basis. Therefore, it’s essential to know your Credit Score before engaging lenders about SBA financing. You can obtain “scored” Credit Reports from any of the three (3) major credit reporting agencies (Experian, Equifax, and TransUnion) or consumer services companies for around $10 or less. Most importantly, requesting your score (“soft pull”) doesn’t reduce your Credit Scores, unlike applying for financing from multiple lenders within a specific period. Consequently, we recommend pulling all three (3) scores since SBA lenders will compare your middle score (throw out the highest and lowest scores) to the 680 benchmark. In addition, most credit reporting services offer credit monitoring and reporting as a packaged solution, and it’s significantly cheaper than recovering a stolen identity.

What kind of businesses qualify?

The SBA limits eligibility to for-profit businesses located in the US, or its territories, with up to 500 employees and no more than $7.5 million in Revenue at any time during the last three years. Additionally, the business’s Net Income and Tangible Net Worth must fall below $5 million and $15 million, respectively. The government also doesn’t permit loans to companies involved in real estate speculation, gambling, or illegal activity, among others. Lastly, the SBA prefers entrepreneurs that are actively involved in the day-to-day activity of the business, so you can’t use the proceeds to invest in securities.

How much money can you get via an SBA Loan?

The amount of the loan will depend on the SBA program, the value of your Assets (business and personal), and your ability to make loan payments or Debt Service.

- Programs: SBA programs fall into two categories: loans requiring third-party intermediaries (the 504 and Micro-loans) and the 7a program, the most popular. The 504 program centers around real estate projects up to $5 million. The program is offered exclusively through SBA Certified Development Corporations (or “CDCs”). Under the Micro-loan program, SBA-approved non-profit entities provide loans up to $50,000. These non-profits tend to focus on historically marginalized groups and borrowers with less than perfect credit. However, working with intermediaries also adds a layer of complexity to a process that often takes longer than conventional (non-SBA) lending. Alternatively, the 7a program doesn’t involve intermediaries and supports loans for real estate, construction, and working capital (critical for new businesses), among other things. We should also note, most banks have a minimum loan amount ($200,000 to $400,000) to offset the fixed costs of making loans. As a result, the SBA developed the 7a “Express” program to encourage smaller loan requests (up to $350,000).

- Assets (Collateral): The SBA requires a 10% Equity contribution from owners. But your Equity injection can also include “soft” costs, such as Franchise Fees, Legal Fees, and other startup costs. As a general rule, if you spent money to start or acquire the business and it isn’t refundable (e.g., lease deposit), you should be able to count it toward your Equity injection. Unfortunately, lenders will disagree about which expenses count toward Equity, and it’s in your best interest to check with your lender before signing a term sheet (i.e., while you have negotiating strength). In addition, approximately 15% to 25% of an SBA loan isn’t government-guaranteed, so lenders will want your Assets (business and personal) and Equity injection to make up the difference.

- Debt Service (Capacity): Capacity relates to the business’s ability to support the Debt payments and the borrower’s post-transaction liquidity. First, the SBA requires a minimum Debt Service Coverage Ratio (“DSCR”) of 1.15 times (“1.15x”). However, DSCR is a minimum requirement, and lenders aren’t interested in clients struggling to service the Debt, so you’ll need a higher DSCR for bank approval. For example, a lender might approve a transaction for a twenty-year-old company with a 1.20x and decline a loan to a new firm with a 1.30x DSCR. Consequently, having consistent payment history is an important consideration of a Capacity assessment. The second measure of Capacity is post-transaction liquidity, which measures the borrower’s ability to make Debt payments in a scenario where the business doesn’t generate Revenue. Here, most banks want to see 6-12 months of post-transaction liquidity. For instance, if your Debt Service is $2,000 per month, then after closing, you should have $12,000 to $24,000 set aside to cover the post-transaction liquidity requirements.

What are the repayment terms?

The maximum repayment term, or maturity, is dependent on the useful life of the business’s Assets. So, you can expect up to twenty-five years for real estate loans (the maximum) and five to ten (5-10) years for working capital, inventory, or equipment loans. However, your lender may include short-term Assets in your twenty-five-year real estate loan if the real estate value supports it.

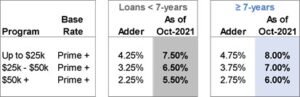

What’s the interest rate for SBA loans?

SBA rates depend on two factors: the base rate (usually the “Prime Rate”) plus an adjustment (or “adder”) based on the useful life of the Asset.

Are there any Fees and Penalties?

The SBA guarantees the first 85% of loans up to $150,000 without any Fees. After that, however, they will assess a 3.0% Guarantee Fee on the 75% of the loans it guarantees from $150,001 to $700,000 and a 3.5% Fee from $700,001 to $3.75 million (75% of $5 million maximum loan amount). So, for example, a $1 million 7a loan would incur about $20,250 in Guarantee Fees (see below) plus an annual Servicing fee of 0.52% of the balance. For loans maturing fifteen (15) years or more, the SBA will assess a prepayment penalty if the loan is refinanced or paid off before maturity. For 7a real estate loans the prepayment penalty is 5.0%, 3.0%, 1.0%, and 0% over the first four years respectively. With the 504 program, the prepayment penalty declines from 3.0% in the first year to 0% in the eleventh year.

Are there any other beneficial considerations that can help increase your loan approval (Character)?

Yes. The SBA generally doesn’t permit refinancing of SBA Debt to take advantage of lower rates. We believe they’ve taken this stance to avoid lenders refinancing loans annually to generate Fee Income. Accordingly, refinancing an SBA loan requires significant documentation, including proof you’ve been declined for conventional refinancing as well as a rationale for modifying (refinancing) your existing SBA Debt. Lenders will also evaluate a prospective borrower’s “Character” before approving financing. Arrests, convictions, tax liens, and judgments will negatively impact your Character assessment. Therefore, we recommend getting these items removed from your “public record” or settled to maximize your chances. Finally, lenders will also generally avoid lending to borrowers with a prior bankruptcy. However, a small handful will overlook a bankruptcy discharged over ten years ago. Please contact us for help with prior bankruptcies.

Why Franchising works well for SBA lending?

Once your lender gets comfortable with your Credit, Capacity, Collateral, and Character, they’ll want to understand how much experience you have in the industry. Of course, the more experience you have, the easier it becomes to get financing. However, if you’re looking for a career or industry change, Franchising is a great way to check the experience box. The Franchising model works well because Franchises with a long history and numerous locations (e.g., KFC, McDonald’s, and Subway) tend to satisfy the Collateral and Capacity requirements of the Four Cs of credit. That’s why Franchising works well for both conventional and SBA lending, and it’s something to keep in mind when considering your options!

We hope you enjoyed this article, and please feel free to contact us with any questions about Franchising or SBA lending.